Will AI-powered bots replace Market Access professionals?

Undeniably, AI is set to revolutionize parts of the market access value chain. But be reassured – there is a future for Market Access professionals.

Undeniably, AI is set to revolutionize parts of the market access value chain. But be reassured – there is a future for Market Access professionals.

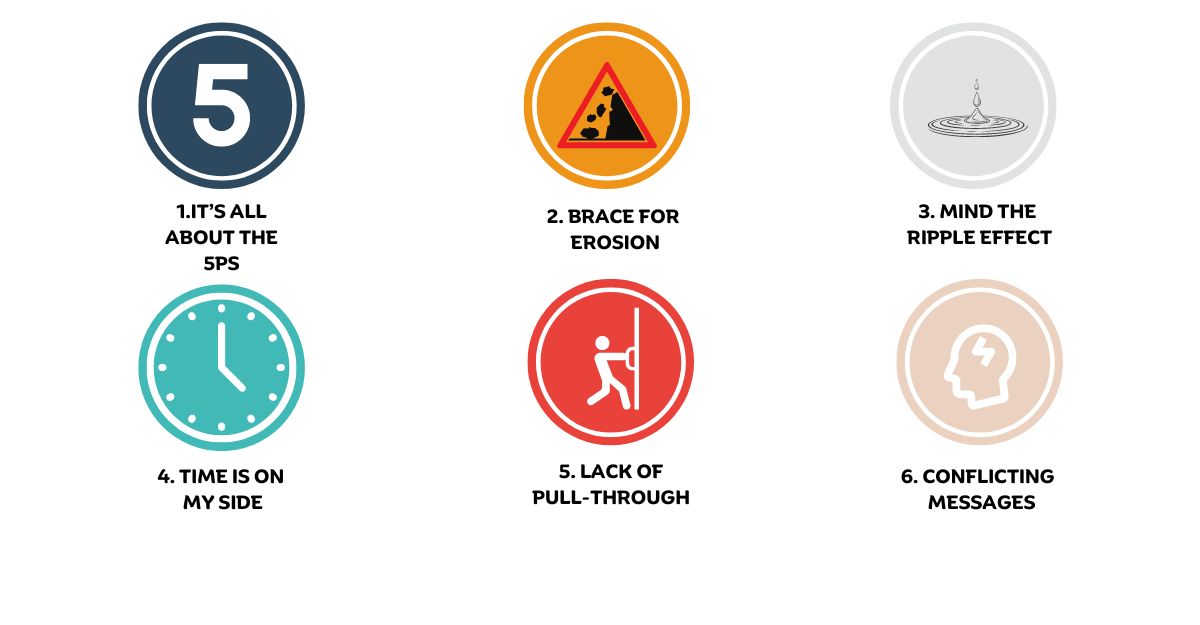

Manufacturers don’t use fast-track reimbursement in Europe. Although this seems like an oversight, there are six reasons explaining why it is not happening.

A strategic market access consultant won’t create a strategy for you but can help a great deal in optimal decision making and saving money down the road. Here are 5 reasons why you need one.

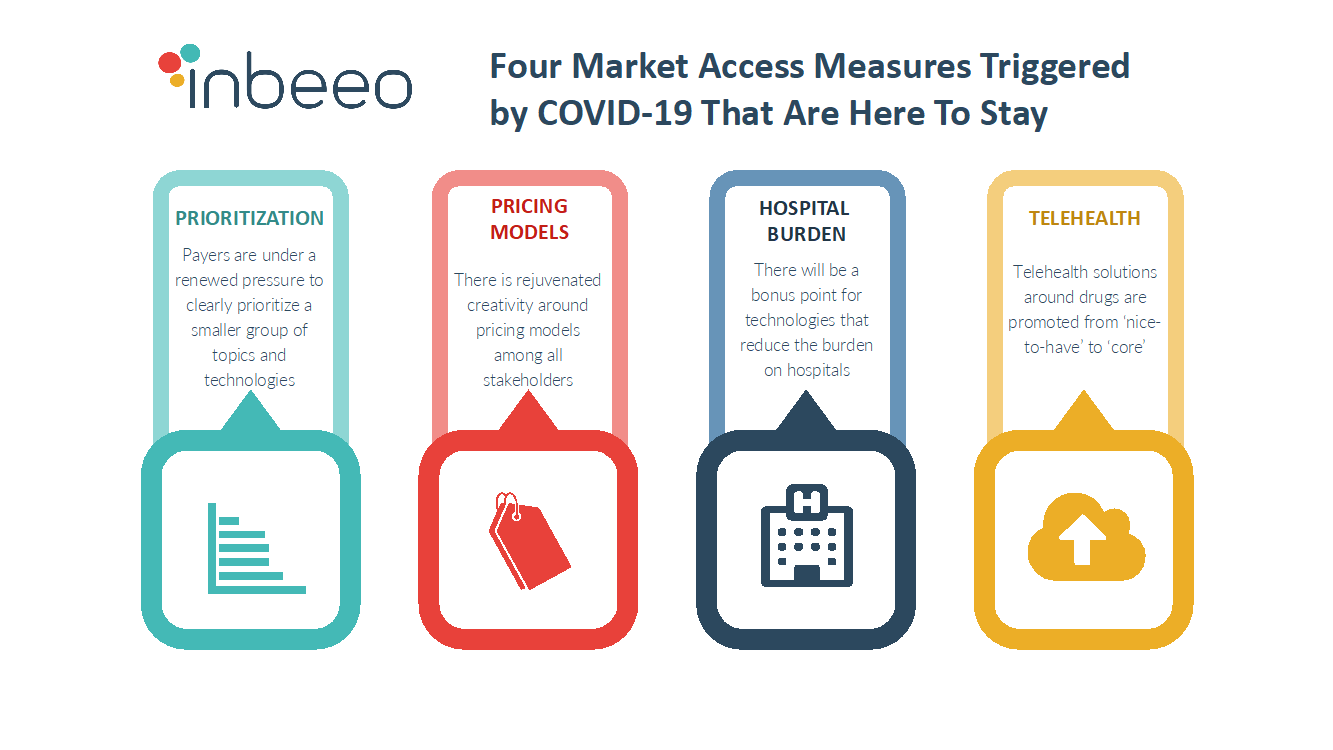

Some initial market access decisions, made during a unique healthcare crisis, hint at lasting changes for pharmaceutical market access.

Inbeeo dives into the data from our COVID-19 Impact on Market Access Activities Dashboard and identifies three positive trends that emerged.

The Challenge Inbeeo’s client, a mid-sized pharma company, was renewing and relaunching their internal Real-World Evidence capabilities as a cross-functional team. They approached Inbeeo to

The Challenge Inbeeo’s client, a specialty pharmaceutical company, was preparing for the Wave 1 launch of an ‘incremental innovation’ product. They required health economic tools

The Challenge Inbeeo’s client, a leader in a specialty CNS area, were actively preparing for the global launch of two products in quick succession. With

The Challenge Inbeeo’s client, a mid-size biopharmaceutical company, were facing challenges in gaining reimbursement for some of their products across Europe. They had begun to

The Challenge The EU regulatory landscape is evolving, with one of the main changes being the introduction of the Joint Clinical Assessment (JCA). The regulation